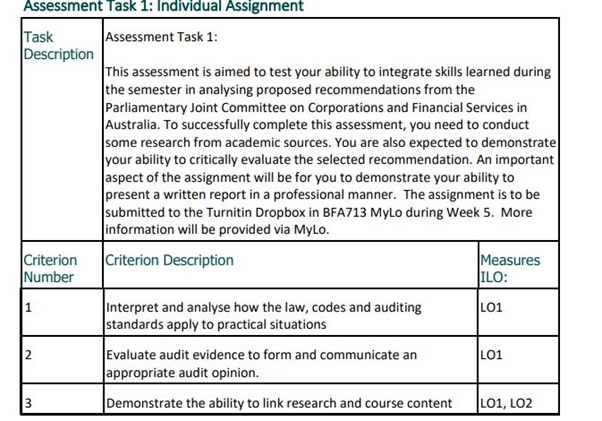

BFA713 Audit & Assurance Individual Assessment

INTRODUCTION

In August of 2019, the Parliamentary Joint Committee on Corporations and Financial Services commenced an inquiry into auditing regulation in Australia. This inquiry was instigated by the ASIC warnings regarding the need to improve audit quality after their audit inspections. Following several submissions from interested parties, an interim report and a final report were formed in 2020 after public hearings held across November and December 2019 (available on MyLO).

Ten recommendations were provided, 1 among which the following were present

| Regulatory Recommendation Summary

|

Background (source: Australian Financial Review)

|

| Recommendation 4: The government to amend the Corporations Act to require auditors confirm they have not provided prohibited non-audit services. | This might be helpful if coupled with a clear list of banned non-audit services (Recommendation 3).

|

| Recommendation 6: The FRC to require companies to disclose audit firm tenure in financial reports by the end of FY2021. | This should bring more transparency for shareholders about the length of the relationship. |

| Recommendation 7: The government to amend the Corporations Act to require companies to go to public tender for auditors every 10 years or, if they do not, explain why in their annual reports.2 | This should bring more transparency for shareholders about the auditor-company relationship.

|

1https://www.afr.com/companies/professional-services/what-the-inquiry-into-audit-qualityrecommended-20201111-p56dr2

2 Final report update for recommendation 7: The original timetable of having this rule in place by 2022 has been abandoned due to the COVID-19 pandemic. Instead, the government has been asked to "consider an appropriate timeline for implementation, taking into consideration the economic climate." The committee added that a "staggered implementation" for the tendering regime would "allow boards sufficient time to establish a strategic response to the recommendation and address concerns raised by the sector regarding current pressures and unintended consequences of a rapid implementation schedule."

For terms of reference, submissions, media releases, public hearings and further information, see: https://www.aph.gov.au/Parliamentary_Business/Committees/Joint/Corporations_and_Financial_Serv ices/RegulationofAuditing

Important links for assignment:

Use this links to find reports as It is very important to follow all the instructions please try to use lecture slides to make this assignment.

ASSIGNMENT REQUIREMENTS

PART A

Select ONE recommendation out of the three listed above and explain in your own words why the recommendation might be of regulatory concern.

- In answering this question, incorporate your understanding of the topic from the initial weeks of the semester. Alternatively, you can also examine additional articles relating to the topic identified in the selected recommendation.

(5 marks)

PART B

For the selected recommendation,

- Identify a article/ paper in a journal relating to the topic covered by the recommendation. Provide a succinct summary of the article.

- Explain if the findings of the article support/ refute the discussion about the potential effectiveness of the proposed recommendation.

- When discussing the articles, avoid detailed explanations referring to the motivation and research design sections. Focus should be on the motivation and findings of the article.

- The article should be from a journal ranked A*/ A according to the ABDC rankings. Access to the journal rankings can be found from the following link: https://abdc.edu.au/research/abdcjournal-quality-list/

- The article should have been published during the last five years (2017 to 2021 inclusive).

(10 marks)

PART C

Provide potential suggestions on the implementation aspect of the recommendation in the Australian audit context, with an example.

- In answering this question, avoid repeating recommendations proposed by the journals selected in Part B. Recommendations will be assessed on their practicality.

(5 marks)

Overall: References in-text and bibliography; Writing Style; Clarity & Structure (5 marks) ADDITIONAL INFORMATION

Length

Maximum 1000 words (+/- 10% is acceptable). Reference list is not included in your word limit.

Value

The assignment is worth a total of 25 marks. This assessment counts for FIFTEEN (15) per cent of the marks for this unit.

Submission

The assignment is to be submitted to the Turnitin Dropbox in BFA713 MyLO by 11.59 pm on Friday, August 12th, 2021.

- The submission must be in Word doc – DO NOT SUBMIT AS A PDF. You need to complete the TSBE assignment cover sheet and attach it to your submission.

General formatting requirements

- Font size 12, 1 ½ line spacing, Times New Roman. The 1000 words include the body of the assignment and footnotes. It excludes cover sheet, title page, appendices, and list of references. Students should not use appendices to circumvent the restrictions on the length of the assignment.

- Late submission will be penalised. Refer to the unit outline for more details.

- Plagiarism will not be tolerated. Refer to the unit outline for more details.

Expert's Answer

Chat with our Experts

Want to contact us directly? No Problem. We are always here for you

Professional

Online Tutoring Services

17,148 Orders Delivered |

4.9/5 5 Star Rating |

748 PhD Experts |

Amazing Features

Plagiarism Free |

Top Quality |

Best Price |

On-Time Delivery |

100% Money Back |

24 x 7 Support |

Get Online

Online Tutoring Services